Award-winning PDF software

Form 8594 for Maryland: What You Should Know

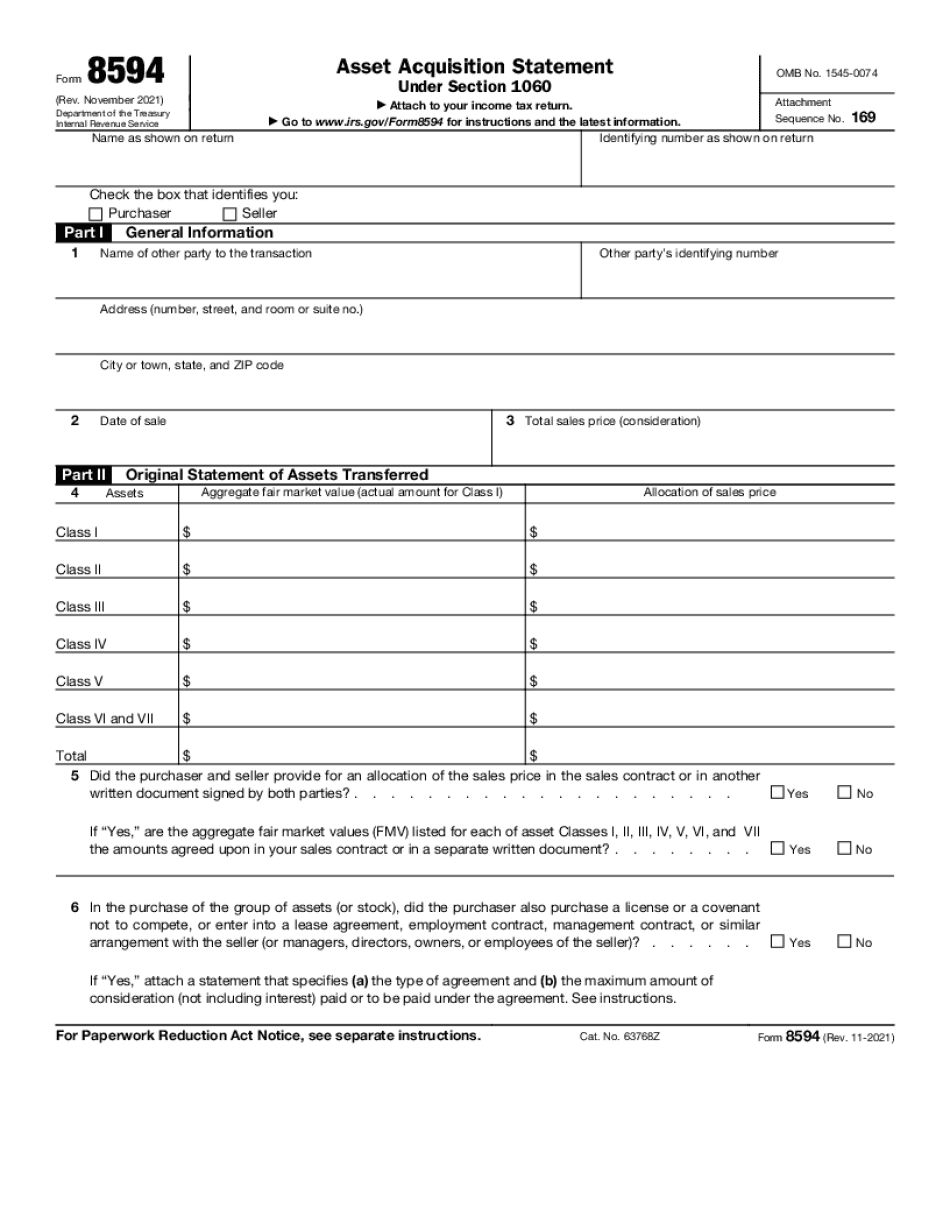

The purpose of this form is to help businesses ensure that they include all their assets, which are typically businesses, in their tax return for that year. To avoid the double filing of tax returns with additional information, you must also attach to Form 8594 an inventory of your business. If you must attach IRS Form 8594 and any supplemental statement to your tax returns … YouTube · ExitReadiness Podcast · Jan 5, 2022 See IRS Form 8594 (Revenue Procedure 2017-50) and your completed tax returns… YouTube · ExitReadiness Podcast · Jan 5, 2022 Understand the Rules for Transfer Taxes and IRS Form 8594. — YouTube · YouTube May 20, 2025 — This report shows you how to determine the applicable tax consequences under tax law for the disposition of assets from a single-stock corporation or a trust or partnership. Generally, these conditions would result in a tax on the transfer of the stock or, in the case of a trust or partnership, the sale of the assets for less than fair value. Under a Section 1250 merger, certain property interests are deemed to be transferred by way of stock dividends (not subject to a gain or loss deduction) and therefore any stock dividend payment becomes a tax event. Under a Section 1250 merger or sale, there are two types of tax consequences: 1. If the stock remains in the original control of the seller of the original stock, the property transferred will be includible in the taxpayer's gross income. However, if the transferred stock is distributed or if stock ownership of the transferor company changes, the tax consequences are substantially different. The amount of the gain or loss will depend on whether the stock was sold for cash or sold at a price higher than the previous market value of the stock. 2. If the stock was sold by the seller as a result of a liquidation, dissolution or winding up, and the distribution of the stock occurred, the stock will not be includible in the taxpayer's gross income for the taxes paid on the distribution (other than the gain or loss), but the loss or gain will generally be subject to the long-term capital gain tax rules. May 23, 2025 — This report shows the difference between the transfer of a stock dividend to shareholders of a single-stock corporation and a cash distribution. For single stocks, the dividend, which generally involves a cash distribution to shareholders, becomes a taxable event for the same tax purpose as if the dividends were made to all shareholders in cash.

Online methods assist you to arrange your doc management and supercharge the productiveness within your workflow. Go along with the short guideline to be able to complete Form 8594 for Maryland, keep away from glitches and furnish it inside a timely method:

How to complete a Form 8594 for Maryland?

- On the web site along with the sort, click Commence Now and go to your editor.

- Use the clues to complete the suitable fields.

- Include your personal info and contact data.

- Make certainly that you simply enter right knowledge and numbers in ideal fields.

- Carefully verify the articles from the type in addition as grammar and spelling.

- Refer to aid portion for those who have any queries or tackle our Assistance team.

- Put an digital signature on your Form 8594 for Maryland aided by the enable of Indicator Instrument.

- Once the form is completed, push Finished.

- Distribute the all set variety by means of e-mail or fax, print it out or help save on the product.

PDF editor allows you to make adjustments with your Form 8594 for Maryland from any world-wide-web connected equipment, personalize it in line with your requirements, indication it electronically and distribute in several methods.